Inventory management is one of the biggest challenges for retail businesses. Statistics say retail business in the U.S. has only 63% of inventory accuracy, leading to stock replenishment errors. Some businesses, especially small ones, still have to use manual inventory operations to have more control over their stock.

In this article, we discuss what retail accounting is and how businesses manage their inventory. We’ll also dive deep into accounting software for retail accounting to help you stay tuned to the best practices.

Key points

- What Is Retail Inventory Management?

- What Is Retail Accounting?

- How Retail Accounting Software Can Help Your Business

- How Does Accounting Software Work?

- Examples of Retail Accounting Software

- What Are the Advantages of Customized Accounting Software?

- What Are the Phases of Retail Accounting Software Development?

- Is It Possible to Migrate All Existing Data to a New Accounting Software?

- Conclusion

What Is Retail Inventory Management?

Let’s start with breaking down the term ‘inventory management’.

Inventory management in retail involves ordering, storing, and selling merchandise.

Managing the products in stock is essential in retail. Knowing inventory key metrics allows businesses to forecast demand and replenish stock timely, plan purchases, track product shortage, manage suppliers, and adjust pricing strategies.

The inventory management process implies 8 key steps. These steps serve as a basis for an inventory management plan.

- Items arrive at your stock location.

- Items get inspected, sorted, and placed in stock according to your storing strategy.

- Monitoring of inventory levels.

- Customers make orders.

- Orders are automatically approved in the POS (point-of-sale) system.

- Items are retrieved from stock and handed to delivery. Updating inventory levels. Items get re-ordered.

This is a basic inventory process flow. Each of these steps can be improved to achieve better results. For example, you can make order management more organized by tracking if the requested item is discontinued or not. This way you can make your replenishment flow streamlined and improve customer experience.

Now, let’s focus on monitoring and updating inventory levels and discover what retail accounting techniques are there to better manage your stock.

What Is Retail Accounting?

The term ‘retail accounting’ can be confusing because this process has little to do with actual business accounting. Retail accounting (or retail inventory) refers to inventory cost calculations. In simple terms, retail accounting helps you to track the value of items you have in stock based on product price and the number of sales.

Here are the most popular techniques to determine the overall item value in the stock.

Weighted average method

The weighted average method considers the average cost of all items purchased in different batches if the price in each batch varies.

Suppose you sell pens. You’ve purchased 100 pens at $0.5 each (one batch) and 100 at $0.7 (another batch). The weighted average method will consider that you have 200 pens with a purchase price of $0.6 in stock.

Weighted average price = Total spendings/total purchased items

The retail method

The retail method is easy to use when you need to calculate the approximate cost of your inventory. The method uses a retail price ratio to calculate the inventory value. It compares the cost and price of the items. All you need to do is subtract the markup from the total value of the products you placed for sale.

Suppose you sell all kinds of stationery with a 30% markup. You know that the total price for all items is $20,000. The markup then will be $20,000 * 0.3 = $6,000. So, your inventory cost is $20,000 – $6,000 = $14,000.

Stock value = the price of all items – markup

NB! The method works well only if your markup for each type of product is the same.

First in, first out (FIFO)

FIFO method, when calculating the cost to acquire, considers that from all the batches you purchased for a given period, you’ll sell items from the oldest one.

Let’s go back to pens. You’ve purchased 100 pens at $0.5 each (one batch) and 100 at $0.7 (another batch). According to the FIFO method, when you sell 20, 30, 40, or less than 100 pens, the total cost is calculated considering the price for the first batch ($0.5 each).

20 pens = $10

30 pens = $15

40 pens = $20

And if you sell 101 pens, the cost will be $50 + $0.7 = $50.7.

These methods can be used for calculating inventory endings for particular purposes. The retail method is good when you need to eliminate the manual count of each item. FIFO is a considerable method for perishable products. The weighted average method can be applied when it’s difficult to track the price of each unit.

How Retail Accounting Software Can Help Your Business

Retail accounting efforts may be minimized due to digitalization. The retail accounting software market is full of solutions that help retail businesses track and manage their inventory.

Standard business accounting applications can be used for accounting purposes if there are features to handle retail-specific tasks. The features are the following:

- retail accounting system connected to a centralized database,

- tax compliant automatic invoicing,

- performance assessment tools,

- supply chain management (order placement and fulfillment, etc.)

- inventory management,

- point-of-sale,

- tax management,

- reporting.

Retail accounting software reduces costs, minimizes human errors, and automates processes. The reasons businesses turn to account software include the ability of the software to:

- forecast and schedule replenishment,

- improve data management,

- generate comprehensive reports,

- connect bank account for seamless payment processing,

- track inventory levels with higher accuracy,

- calculate taxes.

How Does Accounting Software Work?

Retail accounting software may differ in the setup process and have a limited list of features, however, the user experience is straightforward for most of them.

First, you’ll need to create an account and import your business data (clients, goods, expenses, taxes, vendors, etc.). If you use an ecommerce platform (BigCommerce, Shopify, etc.), check the integrations to simplify data import flow. Then you should enter financial preferences and set up online payment.

We suggest following the guidelines offered by software providers. Take time to learn how the features work, and you’re good to go for better accounting.

Examples of Retail Accounting Software

Now, we can look at retail accounting software in detail. Here are the most popular accounting tools.

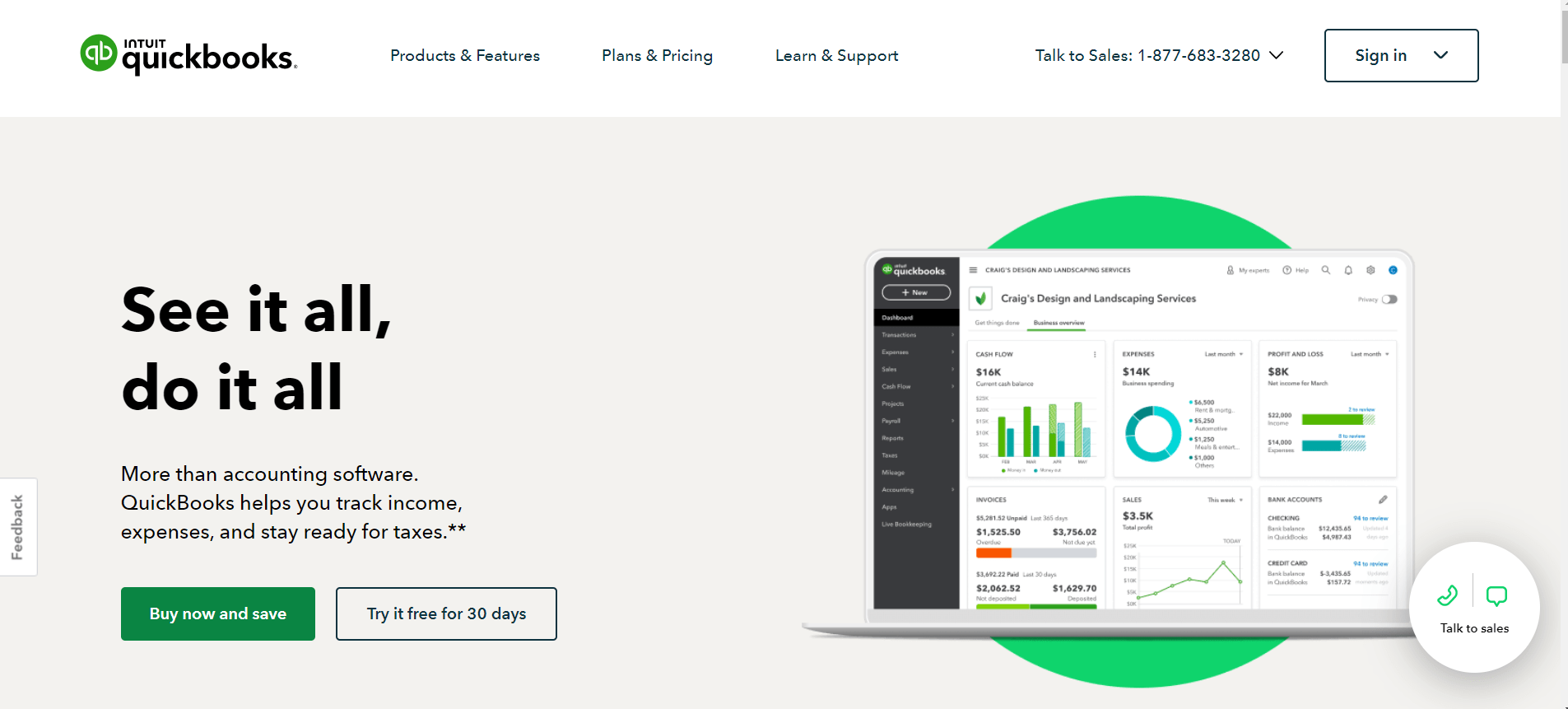

QuickBooks Online

QuickBooks online is one of the most popular accounting software among small businesses. The software offers the features of income tracking, sending invoices and accepting payments, and reporting. Moreover, QuickBooks integrates easily with third-party apps and other QuickBooks solutions to scale your business. Keep in mind that some features (such as inventory management) are available only in the Plus plan.

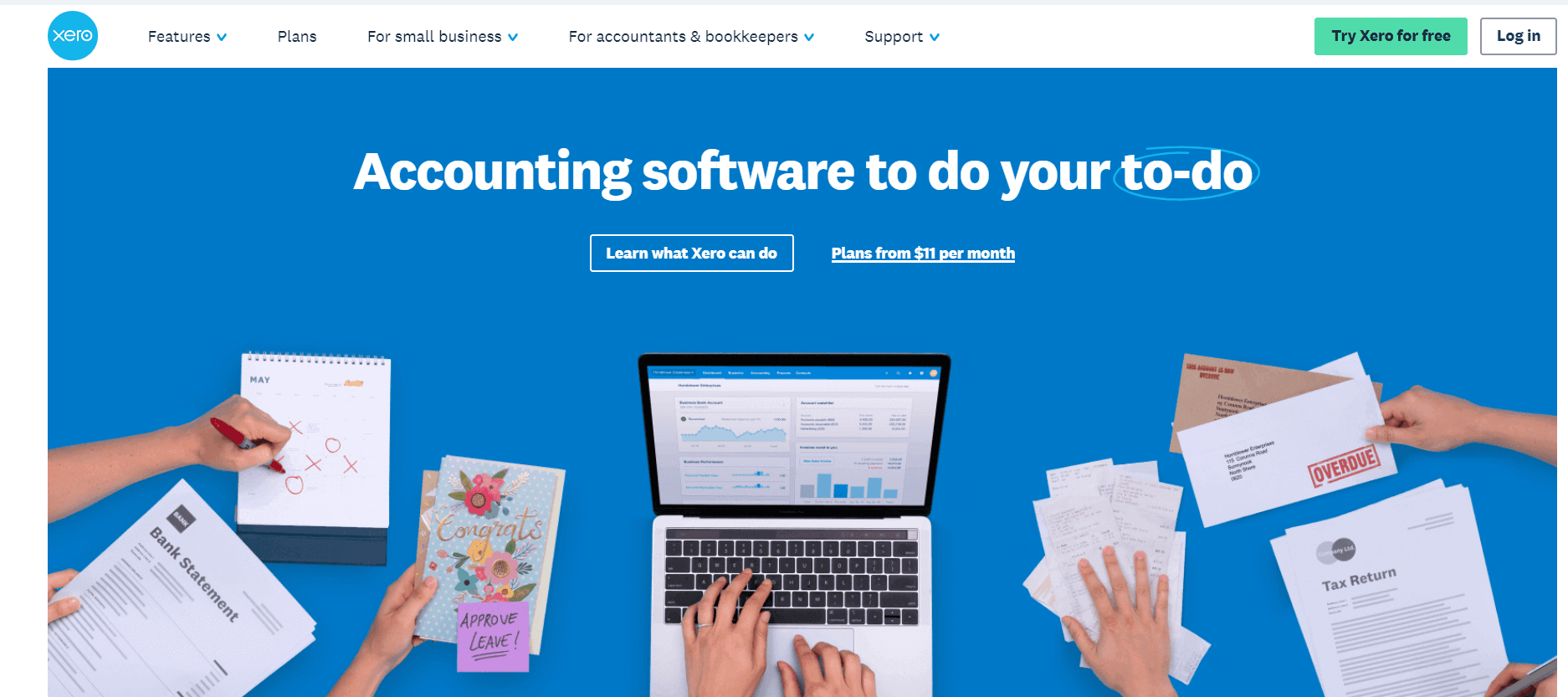

Xero

Xero accounting is a suitable choice for online retail businesses. The software offers inventory management, invoice processing, tax calculations, payments, and reporting in each plan option. It easily connects to the most popular ecommerce platforms. Moreover, you can use a dedicated mobile app for more flexibility.

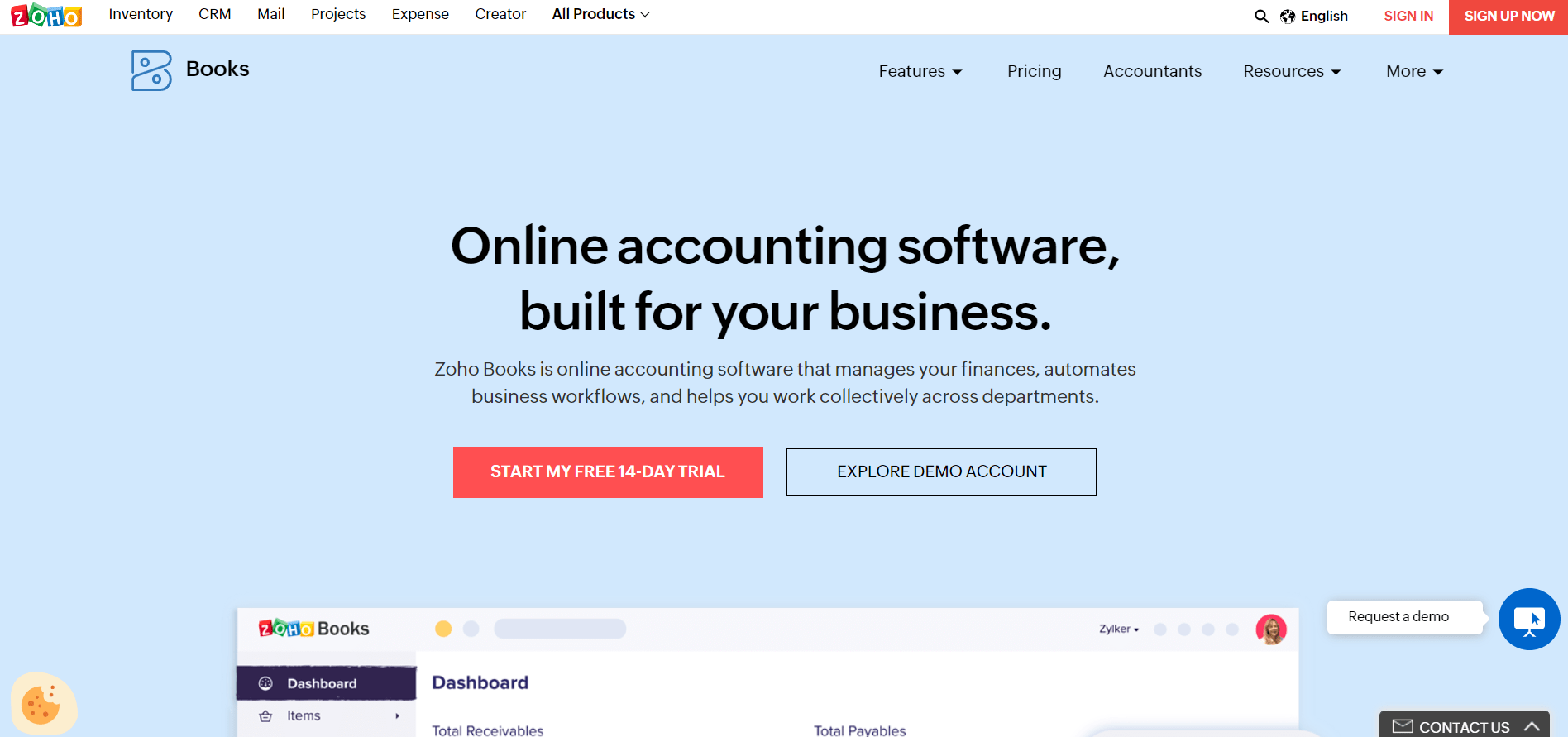

Zoho Books

Zoho Books is a part of a Zoho suite. It works perfectly with Zoho Expenses, Inventory, Analytics, Customer Management system, and more. Features available in Zoho Books include but aren’t limited to:

- Invoices and billing,

- expense tracking,

- reporting,

- budget management,

- order management,

- inventory management

- tax handling.

Compared to Xero and QuickBooks, Zoho Books have limited integration options, however, it’s affordable and can be paired with crucial business tools.

FreshBooks

FreshBooks is a lightweight retail accounting tool with streamlined finance management. The app focuses on creating compliant invoices, online payments, expense tracking, and reporting. For example, FreshBooks automatically keeps a record of payment. The application integrates with tools from 21 categories (PayPal, Acuity Scheduling, HubSpot, etc.)

What Are the Advantages of Customized Accounting Software?

Custom retail accounting software may be a better solution than out-of-the-box tools when your business needs specific features or our business operations have a unique flow. For example, you need to handle your crypto assets but popular tools on the market don’t offer crypto accounting.

Creating custom solutions for accounting purposes gives retailers more flexibility on integrations and digital security. Developers can build a compatible platform to integrate with legacy CRM or other management systems. The same applies to security: if you require advanced protection, IT experts can build robust security features tailored to your needs.

Moreover, custom accounting software is a reasonable choice for businesses that operate within specific local regulations and need their financial operations to be compliant.

If you need a hand in creating a custom retail solution for your business, contact us, and our experts will help you streamline your accounting with the latest technology.

What Are the Phases of Retail Accounting Software Development?

Developing a retail accounting solution requires thorough analysis and planning. Here at Soloway, we break down the development process into 5 steps.

- Problem analysis. An in-depth analysis of your business needs to help us provide you with exact features that solve specific tasks efficiently.

- Solution creation. The process starts with prototyping and UX/UI design to be sure the solution meets your expectations.

- MVP development. After you approve the prototype, our team builds a minimal viable product (MVP) for a quick launch and better testing.

- Product integration. We help you connect the solution with your existing system.

- Support and update. Our professionals stay in touch to support you and maintain the solution.

We strive for long-lasting relationships with our clients and are always glad to talk. If you have any questions about developing software, please, reach out, and our experts will address your questions right away.

Is It Possible to Migrate All Existing Data to a New Accounting Software?

Yes, it’s possible to migrate existing data to a new accounting system. However, the process is delicate and requires thorough preparation so as not to corrupt your business operations. Primarily, you need to define a cut-off date and choose the new accounting system that meets your requirements and is compatible with your hardware. Then, you’ll need to backup existing data, format it, and test imported data.

We suggest you entrust system migration to professionals to minimize errors and quickly restore the functioning of your business.

Conclusion

Retail accounting doesn’t have to be a burden for retailers. Digital solutions such as retail accounting software can automate most of the financial and inventory operations to minimize errors and streamline processes. You can choose an out-of-the-box solution to manage your assets or turn to a software development company to get an efficient solution tailored to your needs. What solution would serve you better? Share your thoughts in the comments below.